Professor, Keio University Faculty of Business and Commerce

Takashi Asano

Financial Accounting, Business Analysis

Assumed current post in 2023, after serving as a Lecturer and Associate Professor at Aichi Shukutoku University and an Associate Professor and full Professor at Tokyo Metropolitan University. Holds a PhD in Business and Commerce from Keio University. Author of numerous books and papers including Sustainability Disclosure Handbook (coauthor, Nihon Keizai Shimbun, 2023), Overcoming ESG Chaos: A Roadmap to Building New Capital Markets (coauthor, Chuo Keizai, 2022), and Accounting Information and Capital Markets: Analysis and Impact of Accounting Change (Chuo Keizai, 2018).

Dynamics of corporate information and capital markets: An empirical approach

Professor, Keio University Faculty of Business and Commerce Takashi Asano

Understanding of fundamental research issues

My expertise is in financial accounting. Financial accounting refer to accounting intended to provide stakeholders with corporate information centered on financial statements. It's also known as accounting for external reporting.

Financial accounting is expected to perform two important functions. The information-provision function provides investors with information useful in making investment decisions and promotes efficient allocation of resources in the capital markets. The interest-adjustment function promotes contractual monitoring and enforcement, lessens conflicts of interest between contractual parties, and makes contracts more efficient. I am particularly interested in these functions, with a focus on the information-provision function.

Investors need information for calculating corporate value and making investment decisions based on the results. Thus the capital markets need information for corporate valuation. Investors value a firm based on forecasts of future performance (i.e., cash flow, dividend, and income) based on corporate valuation models (i.e., the discounted cash flow, dividend discount, and residual income models) rather than past performance. Intentional manipulation of performance, or doubts about its quality, will reduce the forecast accuracy of future performance, and this could reduce the accuracy of corporate valuation.

Interest in nonfinancial information, particularly sustainability information, is rapidly increasing in recent years. While sustainability information is widely recognized to affect medium- to long-term corporate performance, such information lacks clear measurement standards such as accounting standards. This leads to issues concerning its reliability and comparability. For this reason, it is difficult to obtain consistent results on the relationship between sustainability information and corporate value. Research on the value relevance of sustainability information is increasingly valued and actively pursued.

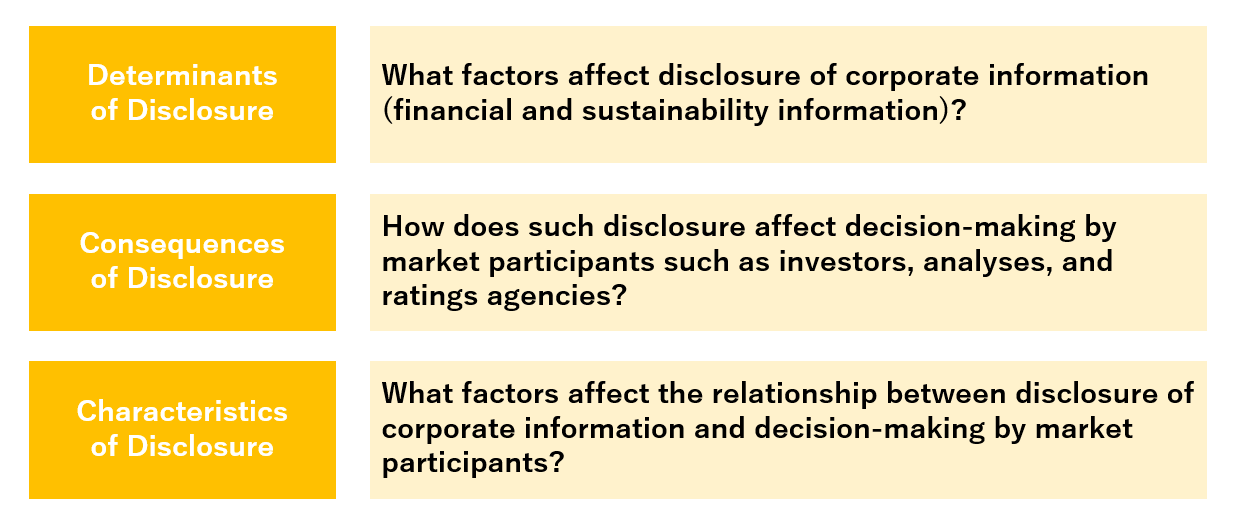

My research theme is “Corporate Information and Capital Markets” focusing on the roles of corporate information in the capital markets. Specifically, I employ empirical methods to analyze (i) what factors affect disclosure of corporate information (such as financial and sustainability information), (ii) how such disclosure affects decision-making by market participants such as investors, analysts, and rating agencies, and (iii) what factors affect the relationship between disclosure of corporate information and decision-making by market participants (Fig. 1).

Research development process

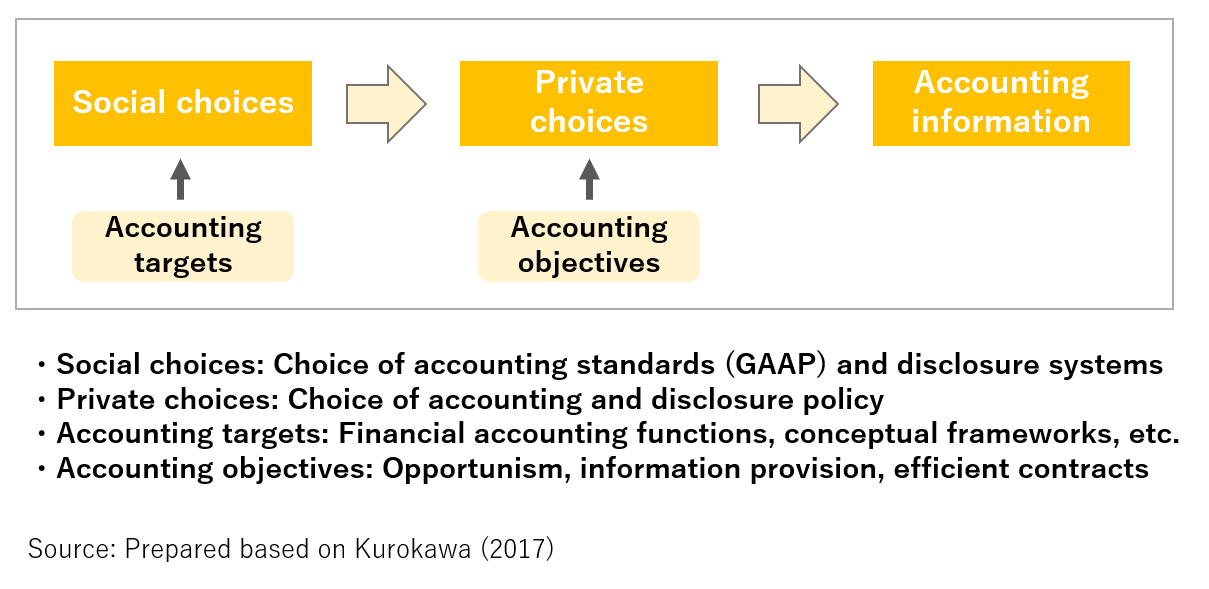

I have conducted empirical analysis of the actual state and impacts of changes in accounting information due to the influence of the International Financial Reporting Standards (IFRS) and other developments. Accounting has been described as a mirror or gauge of the actual state of a company, but that's not all it is. It results from the economic behavior of the individuals creating those facts. In addition, accounting information is a portrayal of certain facets of reality crafted by its makers, essentially a product of fiction.

Under the influence of the IFRS and other developments, room for discretion in accounting and disclosure policy has undoubtedly increased. With a focus on this point, I have observed changes in Japanese accounting and disclosure systems, allowing more room for discretion in accounting and disclosure policy. Through empirical research, I have strived to fairly and objectively explore the following aspects: the accounting objectives guiding companies’ decisions and their subsequent private choices; and whether the changes of accounting information continue to serve accounting objectives, taking into account their private choices (Fig. 2).

The results of these researches were summarized in my 2017 doctoral dissertation titled “Empirical Analysis of Changes in Accounting Information” subsequently earning my doctoral degree. The following year, I published the book “Accounting Information and Capital Markets: Analysis and Impact of Accounting Change” (Chuo Keizai, 2018). While this project demanded time and effort, its culmination led to the receipt of a number of prizes such as the Ota-Kurosawa Prize from the Japan Accounting Association and the Japanese Institute of Certified Public Accountants' Academic Award. I continue my efforts to contribute to society through my research.

In recent years, significant changes have been observed in the capital markets, such as the rise of ESG (environmental, social, and governance) investment and activist investors. These changes also affect corporate information and disclosure. I continue empirical research on “Corporate Information and Capital Markets” incorporating not only traditional financial information but also nonfinancial information such as sustainability information. I strive to adapt to a changing market environment while maintaining consistency in the analytical framework.

Applicability to other fields

In January 2024, I took part in an accounting conference held in China. This conference included sessions on subjects such as accounting, ESG (sustainability), finance, corporate finance, governance, and technology, other related fields, where the latest research were actively presented. As is clear from its session titles, collaboration with other fields is increasingly emphasized in accounting. This trend reflects the fact that accounting is a discipline that chiefly handles information and it is essential to consider its effects on capital markets.

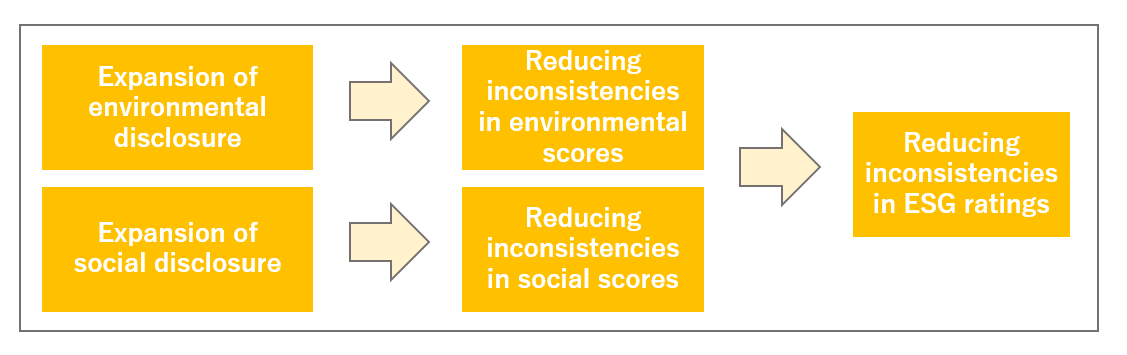

One of the researches I am currently working on is the relationship between sustainability disclosure and ESG ratings. A recent research (Asano 2023) shows that environmental and social score vary among different ESG ratings agencies, leading to increased inconsistency in ESG ratings. In addition, as environmental and social disclosure expands, inconsistency in ESG ratings shows a narrow trend. That is, I show that expansion of environmental and social disclosure is an effective way to narrow inconsistency in ESG ratings (Fig. 3). These findings suggest that active disclosure on environmental and social initiatives has positive effects, and they could have implications for research in other fields as well.

Usefulness of research findings

I am currently involved in a research on human capital disclosure through industry-academy collaboration. I put my knowledge from prior research on “Corporate Information and Capital Markets” to use in this new research. In human capital disclosure, collaboration among departments such as HR, corporate planning, IR, and other sections is required to strategically disclose information and contribute to increasing corporate value. But it is not yet clear what kinds of human capital information are related to corporate value. Human capital disclosure, including information such as gender wage gaps, has only just begun to be disclosed in securities reports. It is expected that the relationship between disclosed information and corporate value will become clearer in the future.

As market environments change rapidly, it is increasingly becoming important to put knowledge from practical insights into research. It seems to me that as a judge of the Nikkei Integrated Report Awards numerous firms are striving to increase corporate value by disclosing a wide range of information to their diverse stakeholders. I would like to put these experiences and knowledge into research. I also am a member of the Accounting Research Subcommittee of the Japan Accounting Association's Next-Generation Accounting Research and Education Committee, and I serve as a reviewer for research support by the Japanese Institute of Certified Public Accountants. I would like to help promote exchange of knowledge in both research and practical fields by assisting in cooperation between academics and practitioners.

Reference

Asano, Takashi (2023). "Expansion of sustainability disclosure and ESG ratings inconsistency." JSRI Journal of Financial and Securities Markets, no. 122, pp. 63-81

Kurokawa, Yukiharu (2017). Accounting and Society: Public Accounting Theory, Keio University Press